Cryptocurrency has become one of the most popular investment options in recent years. With the rise of Bitcoin, Ethereum, and other digital assets, many investors have seen significant profits. However, these profits often come with a tax burden known as Capital Gains Tax. Understanding how to minimize or avoid Capital Gains Tax on cryptocurrency legally is essential for anyone looking to maximize returns in 2026. This guide explores practical, legal, and strategic ways to reduce or avoid Capital Gains Tax on cryptocurrency while staying compliant with tax laws.

What Is Capital Gains Tax?

Capital gains or profits are referred to as having been realized when stock shares or any other taxable investment assets are sold. Capital Gains Tax is a tax imposed on the profit made from selling an asset that has increased in value. In the context of cryptocurrency, it applies when digital assets are sold, traded, or used to purchase goods and services. The difference between the purchase price (cost basis) and the selling price determines the taxable gain.

There are two main types of Capital Gains Tax:

- Short-Term Capital Gains Tax – Applies to assets held for less than one year. These gains are usually taxed at the investor’s regular income tax rate.

- Long-Term Capital Gains Tax – Applies to assets held for more than one year. These gains are typically taxed at a lower rate, encouraging long-term investment.

Understanding these categories is crucial for planning strategies to avoid or reduce Capital Gains Tax on cryptocurrency.

How Capital Gains Tax Applies to Cryptocurrency

Cryptocurrency is treated as property by most tax authorities, including the IRS in the United States and HMRC in the United Kingdom. This means that every time cryptocurrency is sold, traded, or exchanged, it triggers a taxable event. Common taxable events include:

- Selling cryptocurrency for fiat currency (e.g., USD, GBP, EUR)

- Trading one cryptocurrency for another

- Using cryptocurrency to buy goods or services

- Receiving cryptocurrency as payment for work or services

Each of these actions can create a Capital Gains Tax liability. However, there are several legal strategies to minimize or avoid this tax.

Why Avoiding Capital Gains Tax Matters

Avoiding or reducing Capital Gains Tax can significantly increase overall returns on cryptocurrency investments. For example, if an investor sells Bitcoin worth $100,000 that was purchased for $50,000, the $50,000 profit is subject to Capital Gains Tax. Depending on the tax rate, this could mean losing thousands of dollars in taxes. By using smart tax planning, investors can retain more of their profits and reinvest them for future growth.

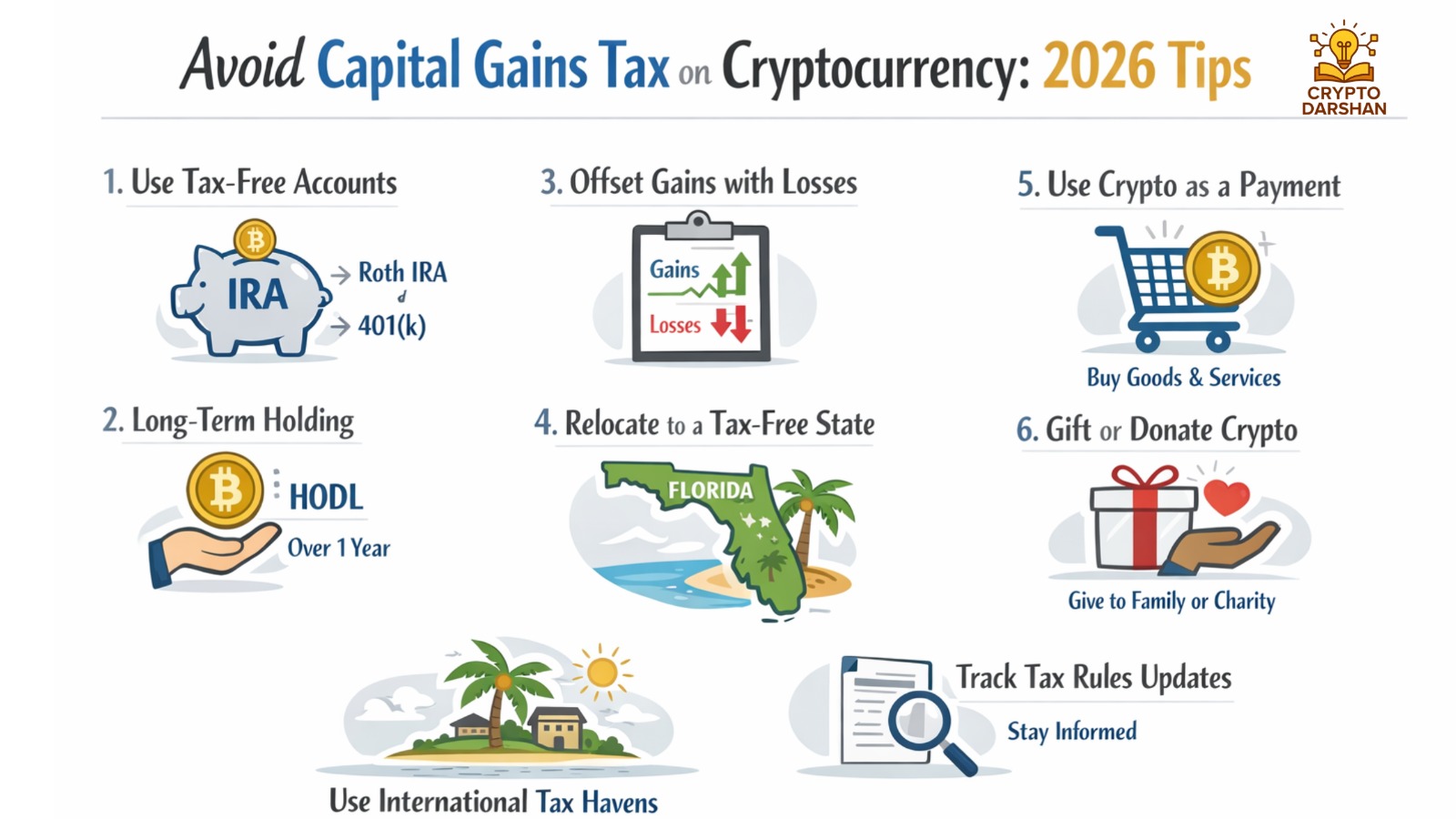

Legal Ways to Avoid Capital Gains Tax on Cryptocurrency

1. Hold Cryptocurrency Long-Term

One of the simplest ways to reduce Capital Gains Tax is to hold cryptocurrency for more than one year. Long-term holdings qualify for lower Capital Gains Tax rates. This strategy not only reduces tax liability but also aligns with the long-term growth potential of digital assets.

2. Use Tax-Free Allowances

Many countries offer tax-free allowances for capital gains. For example, in the UK, individuals have an annual Capital Gains Tax allowance, meaning gains below a certain threshold are tax-free. By strategically selling cryptocurrency within this limit, investors can avoid paying Capital Gains Tax.

3. Offset Losses Against Gains

If some cryptocurrency investments result in losses, these can be used to offset gains from other investments. This process, known as tax-loss harvesting, reduces the overall Capital Gains Tax liability. For instance, selling a losing asset before the end of the tax year can balance out profits from other sales.

4. Donate Cryptocurrency to Charity

Donating cryptocurrency to a registered charity can help avoid Capital Gains Tax. When cryptocurrency is donated directly, the donor does not pay tax on the appreciated value, and the charity receives the full amount. This method benefits both the investor and the charitable organization.

5. Gift Cryptocurrency to Family Members

Gifting cryptocurrency to family members can be another way to reduce Capital Gains Tax. In some jurisdictions, gifts below a certain value are exempt from tax. Additionally, if the recipient is in a lower tax bracket, they may pay less Capital Gains Tax when they sell the asset.

6. Move to a Tax-Friendly Country

Some countries have favorable tax laws for cryptocurrency investors. Nations like Portugal, the United Arab Emirates, and Singapore have little to no Capital Gains Tax on cryptocurrency. Relocating to such jurisdictions can legally eliminate Tax obligations.

7. Use a Self-Directed IRA or Pension Fund

In the United States, investors can use a self-directed IRA to invest in cryptocurrency. Gains within the IRA are tax-deferred or tax-free, depending on the account type. Similarly, in the UK, using a pension fund to invest in crypto can help avoid Capital Gains Tax until retirement.

8. Utilize Stablecoins Strategically

Converting volatile cryptocurrencies into stablecoins can help manage tax exposure. While this may trigger a taxable event, it can also lock in profits and reduce future Capital Gains Tax if done strategically during low-tax years.

9. Invest Through a Company

Setting up a company to manage cryptocurrency investments can offer tax advantages. Corporate tax rates are often lower than personal Capital Gains Tax rates. Additionally, business expenses related to trading can be deducted, reducing taxable income.

10. Use Decentralized Finance (DeFi) Platforms Wisely

DeFi platforms offer opportunities to earn yield without selling assets. By staking or lending cryptocurrency, investors can generate income without triggering Capital Gains Tax. However, it’s important to understand how local tax authorities classify these activities.

Understanding Tax Residency and Its Impact

Tax residency determines where an individual is liable to pay taxes.

Each country has its own rules for establishing tax residency, often based on the number of days spent in the country or the location of primary residence. Changing tax residency to a country with no Capital Gains Tax can be a powerful strategy for cryptocurrency investors.

For example:

- Portugal: No Capital Gains Tax on individual crypto sales.

- United Arab Emirates: No personal income or Capital Gains Tax.

- Singapore: No Capital Gains Tax on cryptocurrency trading.

Before relocating, it’s essential to understand the residency requirements and ensure compliance with both the current and new country’s tax laws.

Tax-Loss Harvesting in Detail

Tax-loss harvesting involves selling assets that have declined in value to offset gains from other investments. This strategy can significantly reduce Capital Gains Tax liability. The process includes:

- Identifying underperforming cryptocurrencies.

- Selling them to realize a capital loss.

- Using the loss to offset gains from other crypto sales.

- Optionally repurchasing the same or similar assets after a waiting period.

This approach allows investors to maintain their portfolio exposure while minimizing Capital Gains Tax.

Using Cryptocurrency for Everyday Purchases

Using cryptocurrency to buy goods or services can trigger Capital Gains Tax because it is considered a disposal of the asset. However, some jurisdictions offer exemptions for small transactions. For example, if the gain from a transaction is below a certain threshold, it may not be taxable. Keeping detailed records of all transactions is essential to ensure accurate reporting and compliance.

Record-Keeping and Reporting

Accurate record-keeping is crucial for managing Capital Gains Tax on cryptocurrency. Investors should maintain detailed records of:

- Purchase and sale dates

- Transaction amounts

- Exchange rates at the time of each transaction

- Wallet addresses and transaction IDs

- Fees paid during transactions

Using crypto tax software can simplify this process and ensure compliance with tax regulations. Proper documentation also helps in case of audits or disputes with tax authorities.

Common Mistakes to Avoid

1. Ignoring Tax Obligations

Many cryptocurrency investors mistakenly believe that digital assets are unregulated or anonymous, so they don’t need to report their transactions. This is a serious error. Tax authorities around the world now treat cryptocurrency as taxable property, and exchanges often share user data with governments. Failing to report crypto income or gains can lead to penalties, interest charges, and even legal action. It’s essential to declare all taxable events, including sales, trades, and crypto payments, to stay compliant and avoid unnecessary trouble.

2. Mixing Personal and Business Assets

Some investors use the same wallets or accounts for both personal and business crypto transactions. This can create confusion when calculating profits, expenses, and Capital Gains Tax. Mixing funds makes it difficult to track which transactions belong to which category, leading to inaccurate reporting. To prevent this, maintain separate wallets and records for personal investments and business activities. Clear separation ensures accurate accounting and simplifies tax filing.

3. Not Tracking Cost Basis

The cost basis is the original value of a cryptocurrency when it was purchased. Without accurate cost basis records, it becomes nearly impossible to calculate the correct Capital Gains Tax. Many investors forget to record purchase prices, transaction fees, or exchange rates, which can lead to overpaying or underpaying taxes. Using crypto tax software or spreadsheets to track every transaction helps maintain precise cost basis data and ensures accurate tax reporting.

4. Assuming Crypto Is Anonymous

While cryptocurrency transactions are pseudonymous, they are not completely anonymous. Every transaction is recorded on the blockchain, which can be traced back to individuals through exchanges or wallet addresses. Tax authorities use advanced tracking tools to identify unreported crypto activity. Believing that crypto transactions are invisible to regulators is a major mistake. Always assume that your transactions are traceable and report them honestly to avoid penalties.

5. Overlooking International Tax Rules

Cryptocurrency is a global asset, but tax laws vary from country to country. Investors who trade or hold crypto across borders often overlook international tax obligations. For example, moving crypto between exchanges in different countries or relocating to a new jurisdiction can trigger tax events. Some nations also require reporting of foreign-held assets. Understanding the tax rules in each relevant country and complying with them prevents double taxation and legal complications.

Future of Capital Gains Tax on Cryptocurrency

As cryptocurrency adoption grows, governments are updating tax regulations to address digital assets. In 2026, more countries are expected to introduce clearer guidelines for Capital Gains Tax on cryptocurrency. Trends to watch include:

- Increased reporting requirements for exchanges

- Stricter enforcement of tax compliance

- Potential introduction of crypto-specific tax rates

- Expansion of tax treaties to cover digital assets

Staying informed about these changes is essential for effective tax planning.

Smart tax planning goes hand-in-hand with proper risk management. If you’re actively trading, understanding position sizing, stop-loss strategies, and profit-taking can significantly impact your taxable gains. Learn how to protect your capital while minimizing unnecessary tax exposure in our guide on risk management in crypto trading.

Expert Tips for Minimizing Capital Gains Tax

1. Plan Sales Strategically

Timing plays a major role in reducing Capital Gains Tax. Selling cryptocurrency during a year when your overall income is lower can place you in a lower tax bracket, which means you’ll pay less tax on your gains. It’s also wise to hold assets for more than one year to qualify for long-term Capital Gains Tax rates, which are usually lower than short-term rates. Planning sales around market conditions and personal income levels helps maximize profits while minimizing tax liability.

2. Use Spousal Transfers

In many countries, transferring assets between spouses is tax-free. This rule can be used strategically to reduce Capital Gains Tax. For example, if one spouse is in a lower income tax bracket, transferring cryptocurrency to them before selling can result in a lower overall tax rate on the gain. It’s a legal and effective way to share tax responsibilities within a household while keeping more of the investment returns.

3. Reinvest Gains

Reinvesting profits into tax-advantaged accounts or other long-term investments can help defer or reduce Capital Gains Tax. In some jurisdictions, reinvesting gains into specific funds or retirement accounts allows investors to postpone paying taxes until withdrawal.

4. Consult a Tax Professional

Cryptocurrency taxation can be complex, and rules often change from year to year. Consulting a qualified tax professional who understands digital assets ensures that you’re using the best strategies to minimize Capital Gains Tax legally. A professional can help identify deductions, exemptions, and timing opportunities that might not be obvious.

Cryptocurrency Tax Software Tools

Several tools can help calculate and manage Capital Gains Tax on cryptocurrency:

- Koinly

- CoinTracker

- TokenTax

- CryptoTaxCalculator

- ZenLedger

These platforms integrate with major exchanges and wallets, automatically tracking transactions and generating tax reports. Discover how new tools are fighting fraud in our article on AI-powered crypto crime detection.

Case Study: Reducing Capital Gains Tax Through Strategic Planning

An investor purchased 5 Bitcoin in 2020 for $10,000 each. In 2026, the price rose to $80,000 per Bitcoin. Selling all 5 would result in a $350,000 gain, subject to Capital Gains Tax. Instead, the investor:

- Sold only 1 Bitcoin to stay within the annual tax-free allowance.

- Donated 0.5 Bitcoin to a registered charity.

- Transferred 1 Bitcoin to a spouse in a lower tax bracket.

- Moved to Portugal before selling the remaining 2.5 Bitcoin.

Through these strategies, the investor legally minimized Capital Gains Tax while maximizing profits.

Cryptocurrency and Inheritance Tax

Cryptocurrency holdings are part of an individual’s estate and may be subject to inheritance tax. Proper estate planning can help reduce both inheritance and Capital Gains Tax liabilities. Strategies include:

- Setting up a trust

- Gifting assets before death

- Using life insurance to cover potential tax liabilities.

Planning ensures that digital assets are passed on efficiently and tax-effectively.

The Role of Stablecoins and DeFi in Tax Planning

Stablecoins and decentralized finance (DeFi) platforms offer innovative ways to manage crypto portfolios. By earning yield through staking or lending, investors can generate income without selling assets, potentially avoiding Capital Gains Tax. However, income from these activities may still be taxable as interest or dividends, depending on local laws.

Cryptocurrency Tax Regulations by Country

| Country | Capital Gains Tax Rate | Crypto-Friendly? |

| United States | 0–37% depending on income | Moderate |

| United Kingdom | 10–20% | Moderate |

| Portugal | 0% for individuals | High |

| Germany | 0% after 1 year | High |

| Singapore | 0% | High |

| Australia | 0–45% | Moderate |

| Canada | 50% of gains taxable | Moderate |

| UAE | 0% | High |

Understanding these differences helps investors choose the best jurisdiction for minimizing Capital Gains Tax.

Preparing for Tax Season

To prepare for tax season and avoid Capital Gains Tax surprises:

- Review all crypto transactions for the year.

- Use tax software to calculate gains and losses.

- Identify opportunities for tax-loss harvesting.

- Consult a tax advisor for personalized guidance.

- File tax returns accurately and on time.

Proper preparation ensures compliance and minimizes tax liabilities.

Frequently Asked Questions (FAQ)

1. What is the capital gains tax on cryptocurrency?

Capital gains tax on cryptocurrency is the tax you pay on profits made from buying and selling digital assets like Bitcoin or Ethereum. If you sell your crypto for more than you paid, the profit is considered a taxable gain.

2. How can I legally reduce crypto capital gains tax in 2026?

You can reduce crypto taxes by using strategies like holding assets long-term, tax-loss harvesting, using tax-free thresholds, moving to crypto-friendly jurisdictions, or utilizing tax-deferred accounts where available.

3. Is holding cryptocurrency long-term tax-efficient?

Yes, in many countries, holding crypto for over a year qualifies for lower long-term capital gains tax rates compared to short-term trading profits.

4. What is tax-loss harvesting in crypto?

Tax-loss harvesting involves selling crypto assets at a loss to offset gains from profitable trades, reducing your overall tax liability.

5. Are crypto-to-crypto trades taxable?

In most jurisdictions, yes. Swapping one cryptocurrency for another is treated as a taxable event and may trigger capital gains tax.

6. Can I avoid taxes by not converting crypto to fiat?

No. Even if you don’t convert crypto to fiat (like USD), transactions such as trading, swapping, or spending crypto can still be taxable events.

Conclusion

Avoiding Capital Gains Tax on cryptocurrency in 2026 requires careful planning, strategic decision-making, and a thorough understanding of tax laws. By holding assets long-term, using tax-free allowances, offsetting losses, donating to charity, and exploring tax-friendly jurisdictions, investors can legally minimize their tax burden. As regulations evolve, staying informed and proactive is the key to maximizing profits while remaining compliant.

Effective tax planning not only preserves wealth but also supports sustainable growth in the rapidly changing world of cryptocurrency. With the right strategies, investors can confidently navigate the complexities of Capital Gains Tax and enjoy the full potential of their digital assets.