Stablecoins vs Traditional Banking represents one of the most significant shifts in modern finance, as digital currencies are quietly redefining how money is stored, transferred, and accessed around the world. For decades, traditional banking has been the backbone of the global financial system. From safeguarding savings to enabling international trade, banks have acted as trusted intermediaries between individuals, businesses, and governments. Yet, beneath this familiar structure, a quiet but powerful transformation is underway. Stablecoins, digital currencies designed to maintain a stable value, are steadily reshaping how money is stored, transferred, and used across borders.

Unlike highly volatile cryptocurrencies such as Bitcoin or Ethereum, stablecoins are pegged to real-world assets, most commonly fiat currencies like the US dollar. This stability makes them practical for everyday use. As adoption grows, stablecoins are no longer just a crypto niche—they are increasingly compared to traditional banking systems themselves.

This article explores the deepening comparison between stablecoins and traditional banking. We will examine how each system works, their strengths and weaknesses, real-world use cases, regulatory challenges, and what this silent revolution means for the future of global finance.

Understanding Traditional Banking

How Traditional Banks Work

Traditional banks operate as financial intermediaries. When individuals deposit money, banks pool these funds and lend a portion to borrowers. This process, known as fractional reserve banking, allows banks to earn interest while supporting economic activity. Customers gain access to payment services, credit facilities, and financial products in exchange for trusting banks with custody of their funds.

Banks are closely tied to central banks, which manage monetary policy, control interest rates, and ensure financial stability. Clearinghouses and correspondent banks further facilitate domestic and international transactions, but these layers also introduce delays and costs.

Strengths of Traditional Banking

Traditional banking has endured for centuries due to several key strengths:

- Established trust: Banks are widely recognized and trusted institutions.

- Deposit insurance: Many governments insure deposits, reducing risk for customers.

- Access to credit: Loans, mortgages, and credit lines support personal and business growth.

- Regulatory oversight: Compliance frameworks protect consumers and prevent systemic collapse.

- Full-service ecosystem: Banks offer savings, investments, insurance, and advisory services.

Limitations of Traditional Banking

Despite these advantages, traditional banking faces persistent challenges:

- Slow settlement times, especially for cross-border payments.

- High transaction and maintenance fees.

- Limited financial inclusion, leaving millions unbanked or underbanked.

- Centralized control, allowing accounts to be frozen or restricted.

- Operational inefficiencies caused by outdated infrastructure.

These pain points create the perfect environment for alternative financial solutions like stablecoins to emerge.

What Are Stablecoins?

Definition and Core Concept

Stablecoins, which can be found through top crypto exchanges, are designed to bridge the gap between the unpredictability of popular cryptocurrencies like Bitcoin (BTC) and the stability required for everyday financial transactions.Stablecoins are blockchain-based digital currencies designed to maintain a stable price by being pegged to an external asset. Most commonly, this asset is a fiat currency such as the US dollar, but some stablecoins are backed by commodities or other cryptocurrencies.

Stablecoins leverage blockchain networks to enable peer-to-peer transfers without traditional intermediaries. Transactions are transparent, immutable, and often settle within minutes.

Types of Stablecoins

Stablecoins can be broadly classified into four categories:

- Fiat-backed stablecoins – Supported by cash or cash-equivalent reserves (e.g., USDT, USDC).

- Crypto-backed stablecoins – Collateralized by cryptocurrencies and overcollateralized to manage volatility.

- Algorithmic stablecoins – Use algorithms to balance supply and demand.

- Commodity-backed stablecoins – Pegged to physical assets like gold.

Among these, fiat-backed stablecoins dominate due to their simplicity, liquidity, and reliability.

“If you want to dive deeper into the types of stablecoins and understand which ones are currently dominating the market, check out our guide Top 5 Stablecoins to Buy in 2026.

Why Stablecoins Matter

Stablecoins bridge the gap between traditional money and blockchain technology. They provide price stability while unlocking benefits such as instant settlement, borderless access, and programmable finance.

The Silent Revolution Explained

The rise of stablecoins is often called a silent revolution because it is transforming the financial system without loud disruption or collapse of traditional banking. Unlike past financial changes that arrived through crises or radical shifts, stablecoins are spreading quietly by solving everyday problems more efficiently.

A Revolution Without Noise

Most financial revolutions come with dramatic headlines. Stablecoins are different. They are not trying to overthrow banks or replace national currencies overnight. Instead, they are slipping into the global financial system by improving how money already works.

People may not even realize they are using stablecoins. Behind many digital wallets, payment apps, remittance platforms, and online marketplaces, stablecoins power transactions in the background.

Driven by Utility, Not Ideology

The growth of stablecoins is not fueled by political movements or anti-bank sentiment. It is driven by practical benefits:

- Faster payments

- Lower transaction costs

- Borderless transfers

- 24/7 availability

Users adopt stablecoins because they work better for specific tasks, not because they want to abandon banks.

Integration Rather Than Replacement

Stablecoins are not building a parallel financial world isolated from banks. Instead, they often connect directly to traditional financial systems through exchanges, payment processors, and regulated issuers.

Many banks and financial institutions now interact with stablecoins for settlement, liquidity management, and cross-border payments. This integration keeps the revolution quiet but powerful.

Gradual Adoption Across Sectors

Stablecoins are expanding across multiple sectors at a steady pace:

- Remittances: Faster and cheaper international money transfers

- Business payments: Instant settlements with global partners

- Freelancer payroll: Reliable payments without banking delays

- Digital commerce: Stable pricing without volatility

Each use case strengthens adoption without triggering sudden disruption.

Why This Shift Matters

Because the change is gradual, it is easy to underestimate its impact. However, silent revolutions often prove the most lasting. Stablecoins are reshaping expectations around speed, cost, and accessibility in finance.

They are not removing banks from the system they are quietly redefining what people expect money to do.

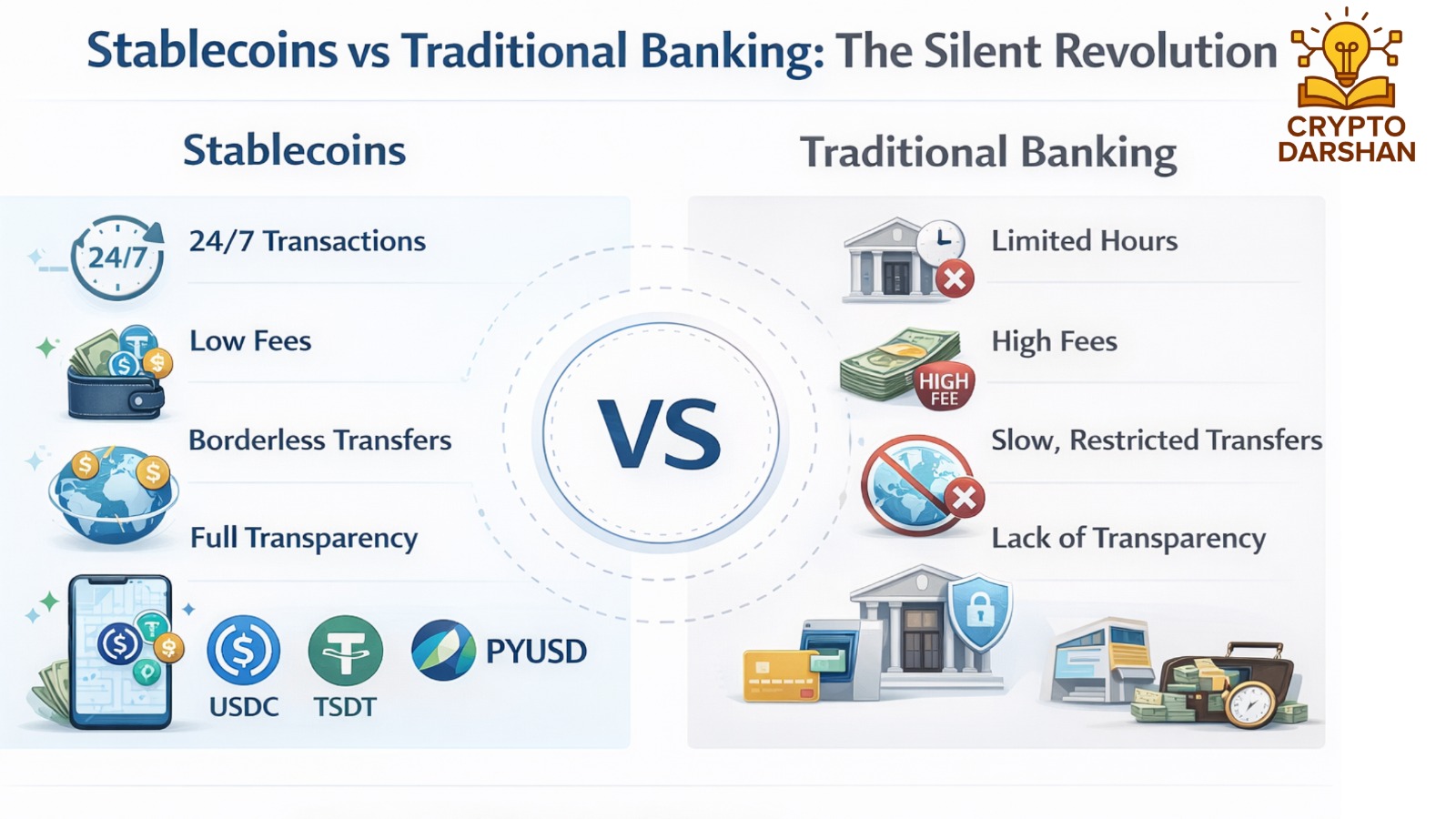

Stablecoins vs Traditional Banking: A Detailed Comparison

Transaction Speed

Traditional banking transactions often require intermediaries, especially for international transfers. This can result in delays of several days.

Stablecoins settle transactions within seconds or minutes, regardless of geography or banking hours.

Cost Structure

Banks rely on fee-based revenue models, charging for transfers, currency exchange, and account maintenance.

Stablecoin transactions usually incur minimal network fees, making them ideal for low-value and high-frequency payments.

Accessibility and Inclusion

Opening a bank account often requires formal identification, minimum balances, and physical presence.

Stablecoins only require a digital wallet and internet access, enabling participation from underserved populations.

Transparency and Trust

Banking operations are largely opaque to customers.

Stablecoin transactions are recorded on public blockchains, allowing real-time verification and auditability.

Custody and Control

Banks maintain custody of customer funds and can impose restrictions.

Stablecoin users retain direct control of their assets, offering financial sovereignty but also greater responsibility.

Comparison Table: Stablecoins vs Traditional Banking

Stablecoins and traditional banks both aim to move, store, and manage money—but they do so in very different ways. Traditional banking relies on centralized institutions and long-established financial infrastructure. Stablecoins, on the other hand, use blockchain technology to enable peer-to-peer transactions without intermediaries.

Below is a detailed comparison across key factors that matter most to users and businesses.

| Feature | Stablecoins | Traditional Banking |

| Transaction Speed | Near-instant (seconds to minutes), 24/7 | Can take hours to days, limited by banking hours |

| Transaction Cost | Very low network fees | Higher fees, especially for cross-border transfers |

| Accessibility | Anyone with a smartphone and internet | Requires documentation, minimum balances, physical branches |

| Geographic Reach | Global and borderless | Restricted by country and banking networks |

| Transparency | Public blockchain records, auditable | Opaque systems, limited customer visibility |

| Custody of Funds | User-controlled (self-custody wallets) | Bank-controlled custody |

| Account Freezing | Difficult unless built into the protocol | Accounts can be frozen by banks or authorities |

| Financial Inclusion | High – serves unbanked and underbanked | Limited access in many regions |

| Regulation Level | Emerging and evolving | Well-established and strict |

| Credit & Loans | Not native (requires DeFi platforms) | Core banking function |

| Security Model | Cryptographic security + user responsibility | Institutional security + consumer protection |

| Operational Hours | Always on (24/7/365) | Limited to business days and hours |

| Trust Model | Trust in code and reserves | Trust in institutions and regulators |

Stablecoins in Global Payments and Remittances

Cross-Border Transfers

Traditional remittance services are costly and slow, often charging high fees for currency conversion and processing.

Stablecoins enable near-instant cross-border transfers at a fraction of the cost, significantly benefiting migrant workers and developing economies.

Business and Enterprise Use

Companies increasingly use stablecoins for international settlements, payroll, and supplier payments. This reduces reliance on correspondent banks and improves cash flow efficiency.

Stablecoins are transforming the way people send money globally and participate in digital commerce. To explore how stablecoins are driving global crypto adoption, read How Stablecoins Are Powering Global Crypto Adoption. For businesses looking to understand the future of online payments with crypto, check How Crypto Is Powering the Future of Online Payment.

Financial Inclusion and Economic Empowerment.

The Global Unbanked Challenge

More than a billion people worldwide lack access to formal banking services due to geographic, economic, or bureaucratic barriers.

Stablecoins as a Gateway

Stablecoins allow individuals to store value, transact globally, and access digital markets using only a smartphone. This empowers entrepreneurs, freelancers, and small businesses in emerging markets.

Regulation: Bridging Innovation and Stability.

Regulation plays a crucial role in shaping the future of both traditional banking and stablecoins. While innovation drives efficiency and accessibility, regulation ensures trust, safety, and long-term stability. The challenge lies in balancing these two forces without slowing progress or exposing users to unnecessary risk.

Why Regulation Is Necessary?

Financial systems affect entire economies. Without proper oversight, risks such as fraud, market manipulation, and systemic collapse can emerge. Traditional banks are heavily regulated because they hold public deposits and influence economic stability.

As stablecoins grow in adoption, they increasingly resemble core financial infrastructure. This makes regulation not just important but essential.

Regulation helps to:

- Protect consumers from fraud and misuse.

- Ensure stablecoin issuers maintain adequate reserves.

- Prevent money laundering and illegal activities.

- Reduce systemic risk to the global financial system

How Traditional Banking Is Regulated?

Banks operate under strict regulatory frameworks set by central banks and financial authorities. These rules govern:

- Capital requirements.

- Liquidity management.

- Customer identification (KYC).

- Anti-money laundering (AML) compliance.

- Regular audits and reporting.

While this oversight builds trust, it also makes banking slow, expensive, and less flexible.

The Regulatory Challenge for Stablecoins

Stablecoins exist at the intersection of technology and finance, which makes regulation complex. Unlike banks, stablecoin issuers may operate globally while being regulated locally—or not at all.

Key regulatory concerns include:

- Reserve transparency: Are stablecoins fully backed?

- Redemption rights: Can users always redeem stablecoins for fiat?

- Issuer accountability: Who is responsible if something goes wrong?

- Jurisdiction issues: Which country’s laws apply?

Without clear rules, both users and institutions face uncertainty.

Regulation as an Enabler, not a Barrier.

Contrary to popular belief, regulation does not necessarily slow innovation. Well-designed regulation can accelerate adoption by providing clarity and confidence.

When governments define clear rules:

- Institutions feel safer adopting stablecoins.

- Businesses gain legal certainty.

- Users develop greater trust.

- Markets become more stable.

This is why many financial experts view regulation as a bridge, not a roadblock.

Toward a Balanced Regulatory Framework.

The ideal regulatory approach does not treat stablecoins exactly like banks—but it does not ignore their risks either. Instead, it recognizes their unique role.

A balanced framework may include:

- Mandatory reserve audits.

- Clear redemption guarantees.

- Consumer protection standards.

- Reasonable compliance requirements.

- Support for innovation and open finance.

Such regulation allows stablecoins to grow responsibly while protecting the broader financial system.

Risks and Challenges of Stablecoins.

Reserve and Transparency Concerns

Users depend on issuers to maintain sufficient reserves, making transparency critical.

Security and User Responsibility

While blockchains are secure, wallet mismanagement and phishing attacks can result in irreversible losses.

Regulatory Uncertainty

Evolving regulations may impact stablecoin availability and usage across jurisdictions.

Are Banks Becoming Obsolete?

At first glance, the rapid rise of stablecoins and digital finance may make it seem like traditional banks are becoming irrelevant. After all, stablecoins allow people to send money instantly, globally, and at very low cost often without needing a bank at all. However, the reality is more balanced and far less dramatic.

Banks are not becoming obsolete, but they are being forced to evolve.

Why Banks Are Still Important?

Traditional banks continue to play a critical role in the global economy for several reasons:

- Credit creation: Banks provide loans, mortgages, and business financing. Stablecoins do not create credit on their own.

- Regulatory trust: Banks operate under strict laws that protect consumers and ensure financial stability.

- Deposit protection: In many countries, bank deposits are insured by governments, offering peace of mind to customers.

- Complex financial services: Services like corporate lending, trade finance, wealth management, and insurance still rely heavily on banks.

These functions cannot be easily replaced by stablecoins or blockchain networks alone.

Where Banks Are Losing Ground?

While banks remain essential, they are losing dominance in certain areas:

- Payments and remittances: Stablecoins move money faster and cheaper than traditional bank transfers.

- Cross-border transactions: Blockchain-based transfers eliminate multiple intermediaries.

- Accessibility: Stablecoins serve people who cannot access banks due to geography or documentation issues.

In these areas, stablecoins are not competing with banks; they are outperforming them.

The Shift from Control to Collaboration

Instead of being replaced, many banks are adapting by embracing blockchain technology. Some are experimenting with:

- Blockchain-based settlement systems

- Digital asset custody services

- Tokenized deposits and bank-issued stablecoins

- Faster cross-border payment rails

This shift marks a transition from centralized control to collaborative infrastructure, where banks and stablecoins coexist.Stablecoins are part of the broader cryptocurrency ecosystem, and understanding Bitcoin can help provide context. Explore the fundamentals in Why Bitcoin Uses Proof of Work Instead of Proof of Stake.

A Hybrid Financial Future

The most likely future is a hybrid financial system:

- Banks continue handling regulation, lending, and large-scale finance.

- Stablecoins handle payments, settlement, and digital transactions.

In this model, stablecoins act as the new rails, while banks remain the institutions of trust.

The Future of Money and Banking

Programmable Finance

Stablecoins enable smart contracts, automated payments, and decentralized applications, redefining how financial agreements are executed.

A More Open Financial System

The convergence of stablecoins and banking could lead to a faster, more inclusive, and transparent financial ecosystem.

Frequently Asked Questions (FAQs)

1. Are stablecoins safer than traditional bank deposits?

Stablecoins and bank deposits offer different types of safety. Bank deposits often come with government insurance, while stablecoins rely on issuer reserves and blockchain security. Each carries its own risks.

2. Can stablecoins replace banks entirely?

Stablecoins are unlikely to replace banks fully. Instead, they complement banking services by improving payment efficiency and accessibility.

3. How do stablecoins maintain price stability?

Most stablecoins maintain stability by holding reserves equal to the value of coins in circulation or through collateral and algorithmic mechanisms.

4. Are stablecoins legal?

In most countries, stablecoins are legal but regulated differently depending on jurisdiction. Regulatory clarity is improving worldwide.

5. What happens if a stablecoin issuer fails?

If reserves are insufficient or mismanaged, users may face losses. This is why transparency and regulation are critical.

6. Do stablecoins earn interest like bank savings accounts?

Stablecoins themselves do not earn interest, but they can be used in financial platforms that offer yield opportunities, often with higher risk.

7. Are stablecoins only used in crypto markets?

No. Stablecoins are increasingly used for payments, remittances, payroll, and business settlements outside crypto trading.

Conclusion: The Silent Revolution in Plain Sight

Stablecoins are not loudly overthrowing traditional banking. Instead, they are quietly reshaping the financial landscape. By offering faster, cheaper, and more accessible alternatives for storing and transferring value, stablecoins challenge long-standing assumptions about money and trust.

Traditional banks continue to play a crucial role in credit creation, regulation, and financial stability. However, the rise of stablecoins signals a shift toward a more open, digital-first financial system.

As regulation matures and adoption accelerates, the boundary between stablecoins and traditional banking will continue to blur. This silent revolution is not about replacement, it is about transformation. The future of finance will be global, programmable, and more inclusive than ever before.

{kind=link}