You open your crypto wallet. You type in an address. You hit send.

In your mind, it feels like a bank transfer. Simple. Fast. Done.

But underneath that one click, something remarkable is happening. Your transaction travels through a web of computers, gets checked by strangers who don’t know you, competes for space inside a digital container, and finally gets locked forever into a chain of data that no one can change.

That process — from your click to permanent record — is one of the most elegant systems in modern technology. And most people have no idea how it works.

This guide is going to change that. We’ll walk through every step of a blockchain transaction in plain language. No jargon walls. No assumptions. Just a clear, honest breakdown of what actually happens inside a block.

What Is a Blockchain, Really?

Before we dive into transactions, let’s make sure we’re on the same page about what a blockchain is.

Blockchain technology is an advanced database mechanism that allows transparent information sharing within a business network. But it’s not like a database at a bank, where one company controls it. Instead, thousands of computers around the world each hold an identical copy of the same database. These computers are called nodes.

Every time new data gets added to this database, it gets packaged into a block. Each block is then chained to the one before it, creating a sequence that goes all the way back to the very first block — called the genesis block.

Because the chain is stored on thousands of computers at once, no single person or company controls it. To change past data, you’d have to alter every copy of the chain on thousands of machines simultaneously. That’s practically impossible, which is what makes blockchains so secure.

Now let’s zoom in on the transaction — the data that gets added to those blocks.

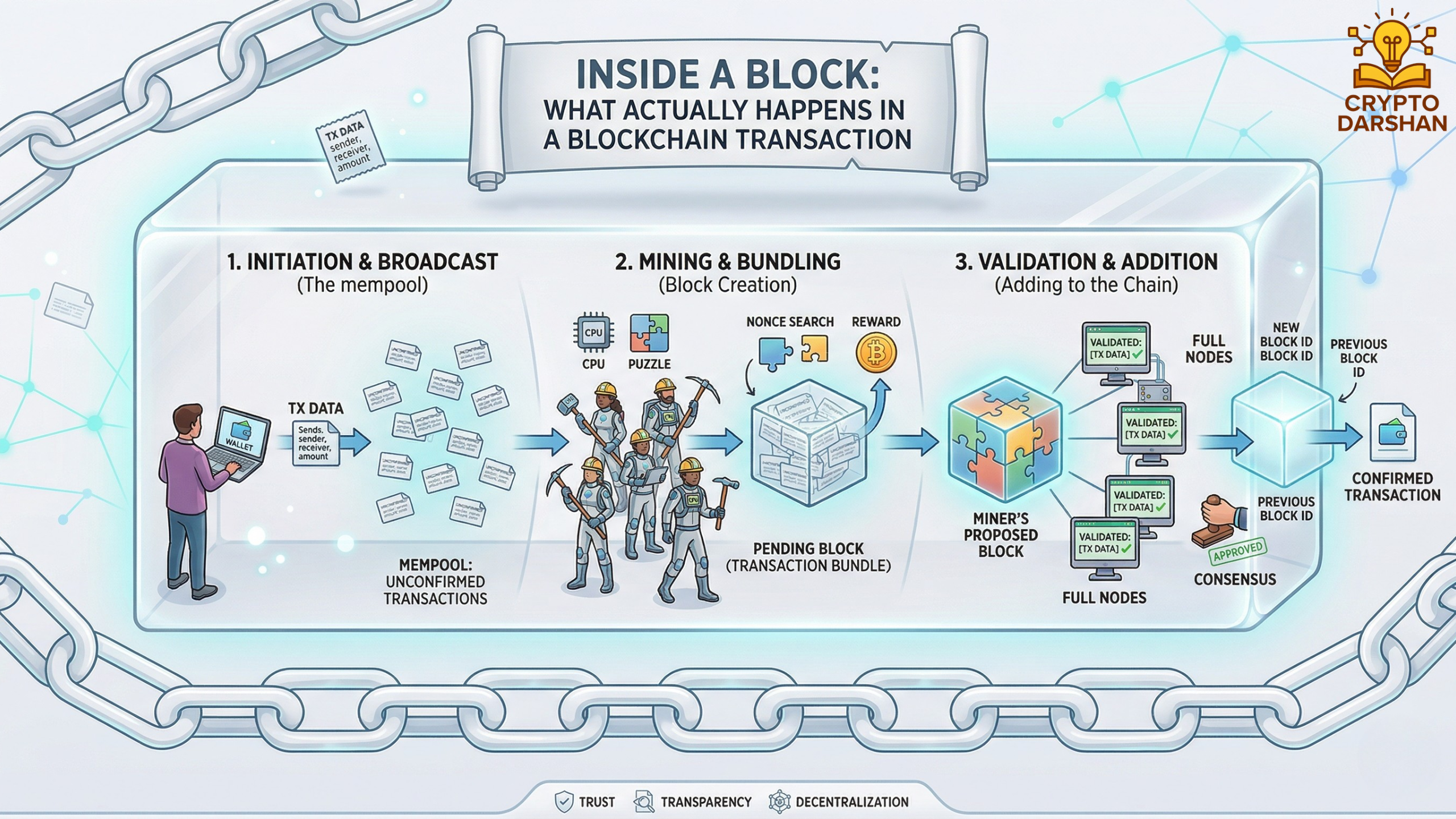

Step 1: You Initiate the Transaction

Every blockchain transaction begins with you.

Let’s say you want to send 0.5 Bitcoin to a friend. You open your wallet app, enter your friend’s public address (a long string of letters and numbers), set the amount, and choose a transaction fee.

Then you click send.

At this point, your wallet does something important: it creates a transaction message. This message contains:

- The sender’s address — your public address

- The receiver’s address — your friend’s public address

- The amount — 0.5 BTC in this case

- A transaction fee — a small payment to incentivize miners or validators

- A reference to past transactions — where your coins came from (more on this below)

This message is not yet confirmed. It’s just a piece of data your wallet has prepared. The real work is about to begin.

Step 2: Your Wallet Signs the Transaction

Here’s where cryptography enters the picture.

Your wallet holds two things: a public key and a private key. Think of the public key as your mailbox address — anyone can see it and send mail to it. The private key is the key to that mailbox — only you have it, and it’s how you prove the mail belongs to you.

When you click send, your wallet uses your private key to digitally sign the transaction. This creates a unique digital signature tied to that exact transaction.

This signature does two things:

- It proves you are the owner of the funds you’re trying to send.

- It locks the transaction data — if anyone tries to change even one digit in the transaction, the signature becomes invalid.

The signed transaction is now ready to be broadcast to the network. Your wallet sends it out like a message in a bottle — dropped into the internet for the network to pick up.

Step 3: The Transaction Enters the Mempool

Your signed transaction doesn’t go straight into a block. First, it lands in something called the mempool.

The mempool (short for memory pool) is a waiting room. It’s a collection of all transactions that have been broadcast to the network but haven’t yet been added to the blockchain. Every node on the network maintains its own version of the mempool.

Right now, at any given moment, the Bitcoin mempool might contain tens of thousands of pending transactions. Ethereum’s mempool holds its own backlog. These are real people and systems waiting for their transactions to be processed.

As blockchain networks grow and transaction volumes increase, analyzing activity within mempools and across the blockchain becomes more complex. This is where advanced analytics tools play an important role. Platforms discussed in Blockchain Analytics Tools: How On-Chain Data Fights Fraud and Crime use on-chain data to track transaction patterns, detect suspicious behavior, and monitor network activity.

While your transaction sits in the mempool, nodes are already checking it. They verify:

- Is the digital signature valid?

- Does the sender actually have enough funds?

- Is the transaction formatted correctly?

If something is wrong, the transaction gets rejected and never makes it into a block. If everything looks good, it stays in the mempool, waiting to be picked up.

Step 4: Understanding Inputs and Outputs (The UTXO Model)

This part trips up a lot of people, but it’s worth understanding.

Bitcoin doesn’t work like a bank balance. Your wallet doesn’t literally hold a number that says “0.5 BTC.” Instead, Bitcoin tracks something called Unspent Transaction Outputs, or UTXOs.

Here’s an analogy. Imagine you have physical cash: a $20 bill and a $5 bill. You don’t have “$25” — you have two specific bills. If you want to pay someone $22, you hand over the $20 and the $5, and you get $3 back as change.

Bitcoin works exactly like this. When you send BTC, your wallet selects UTXOs as inputs — like picking which bills to use. The transaction then creates new outputs: one going to your recipient, and usually one going back to yourself as “change.”

So when someone says a transaction has “inputs” and “outputs,” they mean: which existing coins are being consumed, and which new coins are being created?

This system is clever because it makes transactions easier to verify. A node doesn’t need to track your full account history — it just needs to confirm that the UTXOs you’re spending haven’t already been spent somewhere else.

Ethereum uses a different model called the account model, which works more like a traditional bank balance. But the core logic of proving ownership and preventing double-spending is the same.

Step 5: Miners and Validators Pick Up Your Transaction

Now comes one of the most important parts of the story: who decides which transactions go into the next block?

This depends on which blockchain you’re using.

Proof of Work (Bitcoin)

On Bitcoin, special participants called miners compete to add the next block. They run powerful computers that solve a mathematical puzzle — a process called proof of work. The first miner to solve the puzzle gets to add the next block and earns a reward in Bitcoin.

Miners choose which transactions to include in their block. They almost always prioritize transactions with higher fees, because those fees go directly to the miner. This is why during busy periods on the network, transactions with low fees can sit in the mempool for hours or even days.

Proof of Stake (Ethereum)

On Ethereum (and many other modern blockchains), the system works differently. Instead of miners, there are validators. Validators lock up (“stake”) some of their own cryptocurrency as collateral. The network randomly selects validators to propose and confirm new blocks. If a validator tries to cheat, they lose their staked funds — a punishment called slashing.

Proof of stake uses far less energy than proof of work and is growing in popularity.

Either way, the goal is the same: a set of participants who don’t trust each other reaches agreement on which transactions are valid and in what order they happened. This agreement process is called consensus.

Step 6: Building the Block

Once a miner or validator selects a set of transactions, they start building a block.

A block is essentially a package with two parts: a header and a body.

The Block Body

The body is the straightforward part. It’s a list of all the transactions included in this block. This could be anywhere from a handful to several thousand transactions, depending on the blockchain and the block size limit.

The Block Header

The header is where the magic happens. It contains:

- The previous block’s hash — a unique fingerprint of the block that came just before this one. This is what creates the “chain.”

- The Merkle root — a mathematical summary of all the transactions in this block (explained below)

- A timestamp — when the block was created

- The difficulty target — how hard the proof-of-work puzzle is (for Bitcoin)

- The nonce — a number miners adjust while trying to solve the puzzle

What’s a Hash?

A hash is a fixed-length string of characters produced by running data through a mathematical function. The same input always produces the same hash. But change even one letter in the input, and the hash changes completely.

Here’s why this matters: the block header includes the previous block’s hash. That means if anyone tries to change a transaction in an old block, the hash of that block changes — which breaks its connection to the next block — which breaks that block’s connection to the one after it — and so on, all the way to the present. Every block in the chain would need to be recalculated. That would require more computing power than exists on the network. This is why the blockchain is tamper-proof.

The Merkle Tree

All the transactions in a block are organized into a structure called a Merkle tree.

Picture a family tree, but flipped upside down. At the bottom are individual transactions. Each pair of transactions gets hashed together into a parent hash. Those parent hashes get hashed together. This continues until you have one single hash at the top — the Merkle root.

The Merkle root is a unique fingerprint for all the transactions in the block. If any transaction changes, the Merkle root changes too. And since the Merkle root is stored in the block header, that means the whole block’s hash changes — and the chain is broken.

This elegant structure means you can verify that a specific transaction was included in a block without downloading the entire blockchain. Lightweight wallets use this all the time.

Step 7: Solving the Puzzle (Proof of Work)

For Bitcoin, before a miner can broadcast their block to the network, they have to solve a cryptographic puzzle.

The puzzle: find a number (the nonce) that, when added to the block header data and hashed, produces a result that starts with a certain number of zeros.

There is no clever trick to this. Miners just try billions of random numbers, one after another, until they find one that works. It’s brute force — and it’s intentional. Making the puzzle hard means adding a block takes real-world effort (electricity, computing time). That cost is what prevents spam and makes cheating expensive.

When a miner finds the solution, they immediately broadcast the completed block to the network.

Step 8: The Network Validates the Block

When other nodes receive the new block, they don’t just trust it. They verify it.

Each node independently checks:

- Is the proof-of-work solution valid?

- Are all the transaction signatures correct?

- Are there any double-spends?

- Does the block follow all the rules of the network?

This verification is fast — much faster than mining. Within seconds, thousands of nodes have checked the block and either accepted it or rejected it.

If the majority of the network accepts the block, it gets added to their copy of the blockchain. Your transaction, now inside that block, is officially recorded.

Step 9: Confirmations — Why You Sometimes Have to Wait

When your transaction is included in a block, it gets its first confirmation.

But one confirmation isn’t always enough — especially for large transactions. Here’s why.

Occasionally, two miners solve the puzzle at almost the same time and broadcast two different valid blocks. The network briefly has two competing versions of the chain. This is called a fork.

The rule is simple: the longest chain wins. Miners keep adding blocks to whichever version of the chain they received first. Within a few blocks, one version will pull ahead. The losing chain gets abandoned. Any transactions in those abandoned blocks go back to the mempool to be included in a future block.

This is why many exchanges and merchants wait for multiple confirmations before treating a transaction as final. For Bitcoin, six confirmations (about one hour) is the standard for large amounts. Each confirmation adds another block on top of yours, making it exponentially harder to reverse.

On Ethereum, confirmations work faster — blocks come roughly every 12 seconds, so 12–20 confirmations is usually enough for a high level of security.

Step 10: The Transaction Is Final

After enough confirmations, your transaction is considered irreversible.

No one — not the government, not the developers of the blockchain, not even the person who sent the funds — can undo it. The transaction is sealed into the blockchain, backed by thousands of copies on computers around the world.

Your friend now has 0.5 BTC (minus any change you received back), and that fact is part of an immutable public record that anyone in the world can verify at any time.

What About Transaction Fees?

Transaction fees are a critical part of how blockchains stay running.

When you send a transaction, you attach a small fee. On Bitcoin, this is measured in satoshis per byte (a satoshi is 0.00000001 BTC). On Ethereum, fees are calculated in gas — a measure of how much computational work a transaction requires.

These fees do two things:

- They compensate miners or validators for the work of processing and securing transactions.

- They regulate demand. When the network is busy, fees rise. Users who need fast confirmations pay more. This prevents spam and manages congestion.

During periods of high demand — like a popular NFT drop or a market crash — gas fees on Ethereum can spike dramatically. In 2021, Ethereum gas fees occasionally exceeded $100 for a simple transfer. This drove demand for Layer 2 solutions — secondary networks that process transactions off the main chain and settle them in bulk.

Smart Contracts: Transactions That Do More

So far, we’ve mostly talked about simple value transfers. But blockchains like Ethereum can do something much more powerful: they can run smart contracts.

A smart contract is a piece of code stored on the blockchain. When certain conditions are met, the contract executes automatically — no middleman needed.

For example: a smart contract could say, “If Alice sends 1 ETH to this address before Friday, automatically release the product key.” When Alice sends the ETH, the contract runs, checks the condition, and releases the key — all without a human being involved.

Smart contract transactions work the same way as regular transactions at the network level. They get broadcast to the mempool, picked up by validators, included in a block, and confirmed. The difference is that instead of just moving value, they execute code on every node in the network — ensuring everyone agrees on the result.

Common Misconceptions About Blockchain Transactions

“Transactions are instant.” Not quite. Transactions are broadcast instantly, but confirmation takes time. Bitcoin averages 10 minutes per block. Ethereum takes about 12 seconds. Some blockchains are faster, but true finality always takes at least a few seconds.

“Blockchain transactions are anonymous.” They’re pseudonymous, not anonymous. Your address is a string of characters with no name attached — but all transactions are public. If your address is ever linked to your real identity (as happens on exchanges), your full transaction history becomes visible.

“Blockchain transactions can be reversed if something goes wrong.” This is perhaps the most dangerous misconception. Once a transaction has enough confirmations, it is permanent. Sent to the wrong address? There is no customer service to call. This is why double-checking addresses is so important.

“Every blockchain works the same way.” Not at all. Bitcoin, Ethereum, Solana, Avalanche, and others all have different consensus mechanisms, block times, fee structures, and smart contract capabilities. Understanding the specific blockchain you’re using matters.

The Bigger Picture: Why This Design Matters

You might wonder why all this complexity exists. Why not just have a central database?

The answer is trust — or more precisely, the ability to operate without it.

In a traditional financial system, you trust your bank. You trust that the number on your screen is real, that the bank won’t lose your money, that they won’t freeze your account without reason. That trust is backed by laws, regulations, and insurance.

A blockchain doesn’t require that trust. The math is the guarantee. The rules are written into the code, enforced by thousands of computers, and verified independently by every participant. No one has to take anyone’s word for anything.

That’s a genuinely new idea. And every transaction you send on a blockchain is a real-world demonstration of it.

Inside a Block: What Actually Happens in a Blockchain Transaction (FAQ)

1. What is a blockchain transaction?

A blockchain transaction is the process of transferring digital assets or data from one address to another on a blockchain network. It contains details such as the sender’s address, recipient’s address, amount, timestamp, and a digital signature that verifies the sender’s identity.

2. What happens when a transaction is created?

When a user initiates a transaction, their wallet software creates a transaction request and signs it with a private key. This cryptographic signature proves ownership of the funds and ensures that the transaction cannot be altered after it is created.

3. How is the transaction broadcast to the network?

After creation, the transaction is broadcast to the blockchain network. Nodes (computers connected to the network) receive the transaction and place it in a temporary pool called the mempool, where unconfirmed transactions wait to be processed.

4. How do miners or validators process transactions?

Miners (in Proof-of-Work networks) or validators (in Proof-of-Stake networks) collect transactions from the mempool and group them into a block. They then verify the transactions to ensure that:

- The sender has enough balance.

- The digital signature is valid.

- The transaction follows network rules.

5. What happens during block creation?

Once transactions are verified, they are combined into a block along with other information such as:

- The previous block’s hash

- A timestamp

- A Merkle root (a hash representing all transactions in the block)

This structure ensures the block is securely linked to the blockchain.

6. How does the network confirm the block?

The block must be validated through the network’s consensus mechanism.

- In Proof-of-Work, miners compete to solve a cryptographic puzzle.

- In Proof-of-Stake, validators are chosen based on the amount of cryptocurrency they stake.

Once consensus is reached, the block is added to the blockchain.

7. What are transaction confirmations?

A confirmation occurs when a block containing the transaction is added to the blockchain. Every additional block added after it increases the number of confirmations, making the transaction more secure and difficult to reverse.

8. Why are blockchain transactions considered secure?

Blockchain transactions are secure because they rely on:

- Cryptographic signatures

- Decentralized verification by multiple nodes

- Immutable block structures

- Consensus mechanisms

Together, these features make it extremely difficult to alter or tamper with recorded transactions.

Conclusion: A Small Click, A Complex Journey

Every blockchain transaction is a small miracle of engineering.

From your wallet’s digital signature to the mempool’s waiting room, from the miner’s brute-force puzzle to the validator’s vote, from the Merkle tree’s mathematical summary to the final permanent entry in a global ledger — each step has a purpose, and each purpose builds on the last.

Understanding this process doesn’t just make you more informed about crypto. It helps you make smarter decisions: setting appropriate fees, understanding confirmation times, appreciating why irreversibility is a feature and not a bug, and recognizing the real innovation underneath the price charts and speculation.

As artificial intelligence and blockchain continue to merge, many emerging projects are focusing on advanced data analysis and security applications. Investors and researchers are closely watching the developments highlighted in Top AI Crypto Coins in 2026: Where Smart Money Is Going.