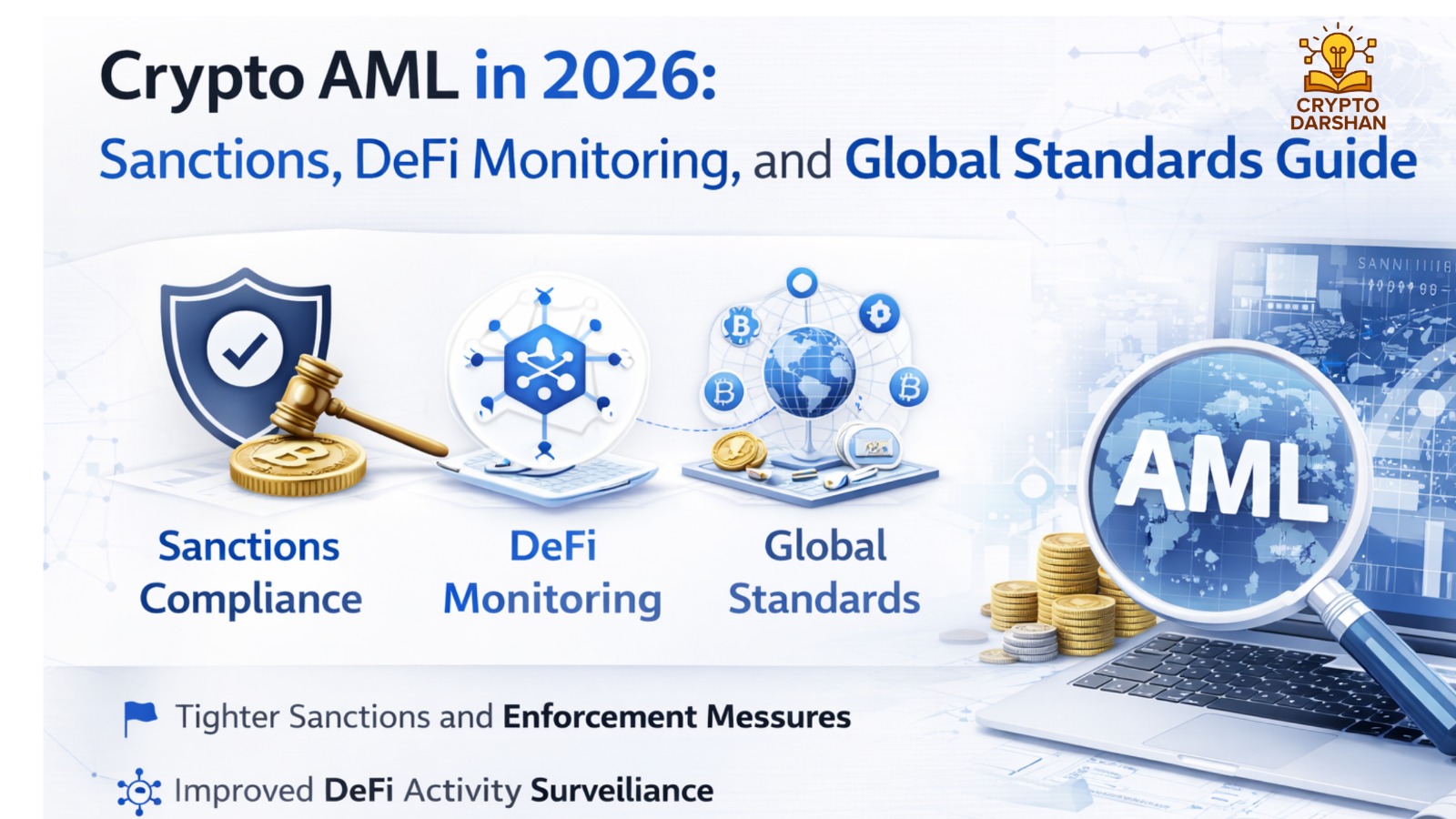

Crypto AML 2026 requires sanctions screening, DeFi monitoring, and global standards compliance amid rising regulations. The year 2026 stands as a defining chapter in the evolution of Anti-Money Laundering (AML) frameworks within the cryptocurrency industry. As digital assets continue to reshape global finance, regulators, financial institutions, and blockchain innovators are converging on a shared mission: to create a transparent, secure, and compliant crypto ecosystem. The rise of decentralized finance (DeFi), the tightening of international sanctions, and the emergence of unified global AML standards have transformed how compliance is managed across borders.

This guide explores the state of crypto AML in 2026, focusing on sanctions enforcement, DeFi monitoring, and the development of global standards. It also examines the role of artificial intelligence, blockchain analytics, and cross-border cooperation in shaping the next generation of compliance strategies.

The Evolution of Crypto AML Regulations

Early AML Challenges in Crypto

In the early years of cryptocurrency, AML compliance was minimal. Bitcoin and other digital assets were often associated with anonymity and illicit activity. Exchanges operated with limited oversight, and regulators struggled to apply traditional financial laws to decentralized systems. The lack of Know Your Customer (KYC) procedures and transaction monitoring tools made it difficult to trace funds or identify bad actors.

The Turning Point: Global Regulatory Awareness

By the mid-2020s, governments recognized the need for coordinated action. The Financial Action Task Force (FATF) introduced the “travel rule” requires VASPs to collect and transmit personal data of both the sender and recipient for transactions. This rule became a cornerstone of crypto AML compliance, prompting exchanges and custodians to adopt identity verification and transaction screening systems.

The 2026 Regulatory Landscape

In 2026, AML regulations for crypto assets are more mature and globally harmonized. Jurisdictions such as the European Union, the United States, Singapore, and the United Arab Emirates have implemented comprehensive frameworks that align with FATF recommendations. The focus has shifted from reactive enforcement to proactive risk management, supported by advanced analytics and blockchain intelligence tools.

The Rise of Risk-Based Supervision

Regulators now emphasize risk-based supervision, where compliance obligations are proportionate to the level of risk a business poses. This approach encourages innovation while maintaining oversight. Smaller startups benefit from simplified compliance pathways, while large exchanges face stricter scrutiny and reporting requirements.

Sanctions Compliance in the Crypto Era

The Growing Importance of Sanctions Screening

Sanctions compliance has become a critical component of crypto AML programs. With geopolitical tensions and economic sanctions expanding, regulators now expect crypto businesses to screen transactions and wallet addresses against global sanctions lists. Failure to comply can result in severe penalties, reputational damage, and loss of operating licenses.

Key Sanctions Authorities

- Office of Foreign Assets Control (OFAC) – Oversees U.S. sanctions enforcement and maintains the Specially Designated Nationals (SDN) list.

- European Union Sanctions Authority – Implements sanctions across EU member states.

- United Nations Security Council – Issues global sanctions targeting terrorism, proliferation, and human rights violations.

- UK Office of Financial Sanctions Implementation (OFSI) – Enforces sanctions within the United Kingdom.

- Asian Sanctions Networks – Emerging regional bodies in Asia coordinate sanctions enforcement across multiple jurisdictions.

Blockchain and Sanctions Evasion

Criminals and sanctioned entities have attempted to use cryptocurrencies to bypass restrictions. Techniques include using privacy coins, mixers, and decentralized exchanges (DEXs) to obscure transaction trails. However, blockchain analytics firms have developed sophisticated tools to trace these activities, linking wallet addresses to sanctioned individuals or entities.

Sanctions Screening Best Practices

- Automated Wallet Screening – Integrate real-time screening tools that flag transactions involving sanctioned addresses.

- Continuous Monitoring – Update sanctions lists automatically to ensure compliance with the latest regulations.

- Enhanced Due Diligence (EDD) – Apply stricter verification for high-risk jurisdictions or counterparties.

- Blockchain Forensics – Use analytics platforms to trace fund flows and identify indirect exposure to sanctioned entities.

- Incident Reporting – Establish protocols for reporting suspicious or blocked transactions to relevant authorities.

- Cross-Chain Sanctions Tracking – Monitor transactions across multiple blockchains to detect hidden exposure.

The Role of AI in Sanctions Compliance

Artificial intelligence now plays a central role in sanctions compliance. Machine learning models analyze transaction patterns, detect anomalies, and predict potential sanctions violations before they occur. These systems reduce false positives and improve the accuracy of compliance operations.

DeFi Monitoring and AML Challenges

The Rise of Decentralized Finance

DeFi has revolutionized financial services by enabling peer-to-peer lending, trading, and asset management without intermediaries. However, its decentralized nature poses significant AML challenges. Smart contracts execute transactions automatically, and users interact through pseudonymous wallets, making it difficult to enforce KYC or monitor suspicious activity.

AML Risks in DeFi

- Anonymity – Users can transact without revealing their identities.

- Cross-Chain Bridges – Facilitate movement of assets across blockchains, complicating traceability.

- Mixers and Tumblers – Obscure transaction origins, often used for laundering funds.

- Flash Loans – Enable rapid, large-value transactions that can be exploited for illicit purposes.

- DAO Governance – Decentralized Autonomous Organizations may lack clear accountability for compliance.

Regulatory Approaches to DeFi AML

Regulators are adapting to DeFi’s unique structure by focusing on “responsible parties” such as developers, front-end operators, and liquidity providers. In 2026, several jurisdictions require DeFi platforms to implement “embedded compliance” — integrating AML controls directly into smart contracts.

DeFi Monitoring Technologies

- On-Chain Analytics – Tools that analyze blockchain data to detect suspicious patterns.

- Decentralized Identity (DID) – Enables users to verify identity while maintaining privacy.

- Smart Contract Auditing – Ensures code integrity and compliance with AML requirements.

- AI-Powered Risk Scoring – Uses machine learning to assess transaction risk in real time.

- Cross-Chain Monitoring – Tracks asset movements across multiple blockchains for comprehensive oversight.

- Compliance Oracles – Smart contract oracles that feed regulatory data into DeFi protocols.

As regulatory tools like blockchain monitoring, AI risk scoring, and AML screening become more advanced, many users feel the ecosystem is becoming harder to navigate — a challenge we explored in detail in our article Are Blockchains Becoming Too Complex for Average Users?

Case Study: DeFi AML Integration

A leading DeFi lending protocol in 2026 implemented a hybrid compliance model combining decentralized identity verification with automated transaction screening. This approach allowed the platform to maintain user privacy while meeting regulatory expectations, setting a precedent for compliant DeFi innovation.

The Future of DeFi Compliance

By 2026, DeFi compliance is evolving toward self-regulating ecosystems. Protocols are adopting governance models that reward users for reporting suspicious activity and penalize non-compliant behavior. This community-driven approach enhances transparency and accountability.

Global AML Standards and Cooperation

FATF’s Role in Global Coordination

The FATF remains the primary body guiding international AML standards. Its recommendations for virtual assets have been adopted by over 200 jurisdictions. In 2026, FATF’s focus includes improving cross-border data sharing, harmonizing Travel Rule implementation, and addressing DeFi and privacy-enhancing technologies.

Regional AML Frameworks

- European Union (MiCA and AMLD6) – The Markets in Crypto-Assets Regulation (MiCA) and the Sixth Anti-Money Laundering Directive (AMLD6) establish comprehensive rules for crypto service providers.

- United States (FinCEN and SEC) – FinCEN enforces AML obligations for exchanges and custodians, while the SEC oversees token offerings and securities compliance.

- Asia-Pacific (Singapore, Japan, South Korea) – These countries lead in implementing risk-based AML frameworks for digital assets.

- Middle East (UAE, Bahrain) – Emerging crypto hubs with strong regulatory oversight and licensing regimes.

- Africa (Nigeria, South Africa, Kenya) – Rapidly developing AML frameworks to support growing crypto adoption.

The Push for Global Interoperability

Global interoperability is essential for effective AML enforcement. In 2026, regulators and industry groups are developing standardized data formats and APIs to facilitate secure information exchange between VASPs. This collaboration enhances transparency and reduces compliance fragmentation.

The Role of Public-Private Partnerships

Public-private partnerships (PPPs) have become a cornerstone of AML innovation. Governments, financial institutions, and blockchain analytics firms collaborate to share intelligence, identify emerging threats, and develop best practices. These partnerships accelerate the detection of illicit activity and strengthen the overall integrity of the crypto ecosystem.

In some cases, poorly regulated token launches can become entry points for unverified funds, which is why strong AML monitoring and regulatory collaboration are becoming essential — a dynamic we explored in our article The Hidden Economics Behind Token Launches.

The Emergence of Global AML Data Networks

New global AML data networks allow real-time sharing of suspicious activity reports (SARs) across jurisdictions. These systems use encryption and privacy-preserving technologies to protect sensitive data while enabling faster cross-border investigations.

How Technology Is Strengthening Crypto AML Compliance

Artificial Intelligence and Machine Learning

AI and machine learning are transforming AML compliance by automating risk detection and reducing false positives. Algorithms analyze transaction patterns, user behavior, and network relationships to identify anomalies indicative of money laundering or sanctions evasion.

Blockchain Analytics Platforms

Companies like Chainalysis, Elliptic, and TRM Labs provide blockchain intelligence solutions that trace transactions across multiple blockchains. These tools enable compliance teams to visualize fund flows, assess counterparty risk, and generate audit-ready reports.

RegTech Integration

Regulatory technology (RegTech) solutions streamline compliance workflows by integrating KYC, transaction monitoring, and reporting into unified platforms. In 2026, many crypto businesses use cloud-based RegTech systems that automatically adapt to regulatory updates.

Privacy-Preserving Compliance

Balancing privacy and compliance is a major focus in 2026. Zero-knowledge proofs (ZKPs) and homomorphic encryption allow verification of user data without exposing sensitive information. These technologies enable privacy-preserving KYC and AML processes that align with data protection laws.

Smart Contract Compliance Automation

Smart contracts can now include built-in compliance logic, automatically enforcing AML rules such as transaction limits, risk scoring, and sanctions screening. This innovation reduces manual intervention and ensures consistent adherence to regulations.

Quantum-Resistant Compliance Systems

With the rise of quantum computing, crypto AML systems are adopting quantum-resistant encryption to secure sensitive compliance data. This ensures long-term protection of transaction records and identity information.

Risk Management and Governance

Building a Risk-Based AML Framework

A risk-based approach tailors AML controls to the specific risks faced by a crypto business. Key steps include:

- Risk Assessment – Identify exposure to money laundering, terrorism financing, and sanctions risks.

- Customer Due Diligence (CDD) – Verify customer identities and assess risk profiles.

- Ongoing Monitoring – Continuously review transactions and update risk assessments.

- Reporting and Recordkeeping – Maintain detailed records for regulatory audits.

- Training and Awareness – Educate employees on AML obligations and red flags.

Governance and Accountability

Strong governance ensures that AML responsibilities are clearly defined. Boards and senior management must oversee compliance programs, allocate resources, and ensure independent audits. In 2026, regulators increasingly hold executives personally accountable for AML failures.

Third-Party Risk Management

Crypto businesses often rely on third-party service providers for KYC, custody, or analytics. Effective oversight includes conducting due diligence, reviewing service-level agreements, and monitoring vendor performance to ensure compliance integrity.

ESG and AML Integration

Environmental, Social, and Governance (ESG) principles are now integrated into AML frameworks. Ethical compliance practices, transparency, and responsible innovation are key factors in building trust with regulators and investors.

Enforcement Trends and Case Studies

Increased Regulatory Enforcement

Regulators worldwide have intensified enforcement actions against non-compliant crypto entities. Penalties include fines, license revocations, and criminal charges. The focus has shifted from small exchanges to major players and DeFi protocols.

Notable Enforcement Cases

- Exchange Sanctions Violations – A major exchange was fined for processing transactions linked to sanctioned Russian entities.

- DeFi Protocol Breach – A decentralized platform faced enforcement for failing to implement AML controls, leading to illicit fund flows.

- NFT Marketplace Investigation – Authorities investigated NFT platforms for facilitating money laundering through high-value art sales.

- Stablecoin Issuer Scrutiny – Regulators examined stablecoin issuers for inadequate AML and reserve transparency.

Lessons Learned

- Compliance by Design – Integrate AML controls from the start of product development.

- Transparency and Cooperation – Engage proactively with regulators.

- Continuous Improvement – Regularly update compliance frameworks to reflect evolving risks.

- Cross-Border Coordination – Collaborate with international regulators to prevent jurisdictional loopholes.

The Future of Crypto AML

Convergence of Traditional and Digital Finance

By 2026, the line between traditional finance and crypto has blurred. Banks now offer digital asset services, and crypto firms adopt banking-grade compliance standards. This convergence fosters greater trust and mainstream adoption.

Global AML Harmonization

Efforts to harmonize AML standards are accelerating. A unified global framework could emerge by 2030, enabling seamless compliance across jurisdictions and reducing regulatory arbitrage.

The Role of Central Bank Digital Currencies (CBDCs)

CBDCs introduce new AML opportunities and challenges. Their programmable nature allows for built-in compliance features, but cross-border interoperability remains a concern. Collaboration between central banks and crypto regulators is essential.

Ethical and Privacy Considerations

As surveillance capabilities expand, balancing AML enforcement with individual privacy rights becomes critical. Transparent governance, ethical AI use, and privacy-preserving technologies will define the next phase of AML evolution.

The Rise of Self-Regulating Crypto Ecosystems

In 2026, self-regulating ecosystems are emerging where compliance is enforced through community consensus and smart contract governance. These systems reward compliant behavior and penalize violations automatically, reducing reliance on centralized authorities.

Best Practices for Crypto Businesses in 2026

- Adopt a Comprehensive AML Policy – Align with FATF and local regulations.

- Implement Advanced Analytics – Use AI and blockchain intelligence for real-time monitoring.

- Ensure Sanctions Compliance – Integrate automated screening and reporting systems.

- Engage in Industry Collaboration – Participate in information-sharing networks.

- Prioritize User Education – Promote awareness of compliance responsibilities.

- Audit and Review Regularly – Conduct independent audits to identify gaps.

- Leverage Privacy-Preserving Tools – Maintain compliance without compromising user data.

- Stay Ahead of Regulatory Changes – Monitor global developments and adapt swiftly.

- Adopt ESG-Aligned Compliance – Integrate ethical and sustainable practices into AML programs.

- Invest in Continuous Innovation – Use emerging technologies to enhance compliance efficiency.

Frequently Asked Questions (FAQ)

1. What is Crypto AML and why is it important in 2026?

Crypto AML (Anti-Money Laundering) refers to regulatory frameworks and compliance processes designed to prevent illegal financial activities such as money laundering and terrorist financing in cryptocurrency transactions. In 2026, it is critical because digital assets are increasingly integrated into global finance and regulators are tightening compliance standards for crypto companies.

2. What role does the Financial Action Task Force play in crypto AML?

The Financial Action Task Force (FATF) sets global standards for preventing money laundering and terrorist financing in virtual assets. It provides guidelines for Virtual Asset Service Providers (VASPs), including licensing requirements, AML controls, and the implementation of the Travel Rule for transaction transparency.

3. What are crypto sanctions and how are they enforced?

Crypto sanctions are restrictions imposed by governments to prevent sanctioned individuals, organizations, or countries from using cryptocurrency networks. Exchanges and crypto businesses must screen wallet addresses and users against sanctions lists and block transactions linked to sanctioned entities.

4. What is the Travel Rule in crypto compliance?

The Travel Rule requires crypto platforms to collect and share sender and receiver information for digital asset transfers. Many jurisdictions now require Virtual Asset Service Providers to implement this rule to increase transparency and reduce illicit financial activity.

5. How are regulators monitoring DeFi platforms for AML compliance?

Regulators are working to bring decentralized finance (DeFi) under AML oversight by identifying responsible entities such as developers or operators and applying compliance obligations similar to traditional financial institutions.

6. Why are stablecoins a growing concern for AML regulators?

Stablecoins are widely used in crypto transactions due to their price stability and liquidity, making them attractive for illicit activities such as money laundering and sanctions evasion. Regulators are increasingly focusing on monitoring stablecoin transactions and wallet activity.

7. What tools do crypto companies use for AML monitoring?

Crypto firms use blockchain analytics platforms, transaction monitoring systems, and machine-learning models to track suspicious wallet activity, identify laundering patterns, and assess risk scores for addresses involved in transactions.

8. How compliant are countries with global crypto AML standards?

Compliance levels vary globally. As of 2025, only about 40 of 138 jurisdictions assessed were largely compliant with international crypto AML standards, highlighting significant regulatory gaps.

9. What penalties can crypto companies face for AML violations?

Crypto exchanges and financial service providers that fail to meet AML requirements may face heavy fines, regulatory enforcement actions, and loss of licenses. Recent enforcement actions against major platforms show that regulators are increasingly strict about compliance.

Conclusion

Crypto AML in 2026 represents a mature, technology-driven, and globally coordinated ecosystem. The integration of sanctions compliance, DeFi monitoring, and international standards has elevated the industry’s credibility and resilience. As digital assets continue to evolve, the balance between innovation, regulation, and privacy will shape the future of financial integrity.

The path forward lies in collaboration — between regulators, businesses, and technology providers — to ensure that the promise of blockchain innovation aligns with the principles of transparency, accountability, and trust.