The world of corporate finance is undergoing a seismic shift as cryptocurrency continues to move from the fringes of speculation into the mainstream of business operations. For years, companies holding digital assets on their balance sheets faced a major crypto accounting dilemma: how to accurately reflect the value of volatile crypto holdings under traditional accounting standards. The Financial Accounting Standards Board (FASB) has now introduced a groundbreaking rule that changes everything—requiring companies to measure crypto assets at fair value instead of cost basis.

This change, effective for fiscal years beginning after December 15, 2024, marks a pivotal moment for CFOs, accountants, and financial controllers. It not only alters how crypto assets are reported but also impacts earnings volatility, investor transparency, and strategic decision-making. As institutional exposure to Bitcoin expands through regulated investment vehicles, corporate treasury strategies are evolving alongside trends explored in BlackRock, ETFs, and the Institutionalization of Bitcoin.

This comprehensive guide explores the difference between fair value and cost basis, the implications of the new FASB rule, and what every CFO needs to know to prepare for this new era of crypto accounting.

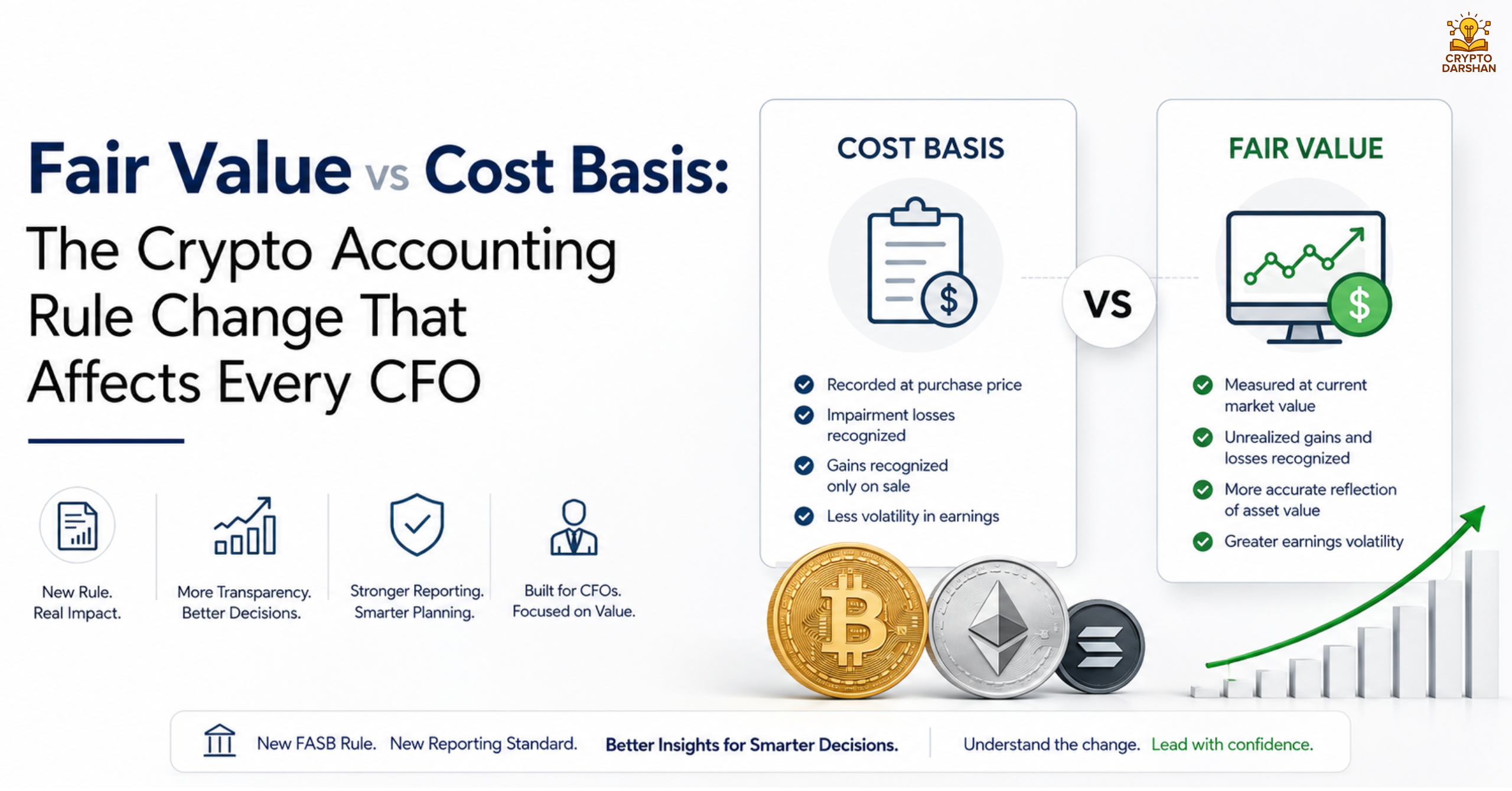

Understanding the Basics: Fair Value vs Cost Basis

What Is Cost Basis Accounting?

Under the cost basis method, assets are recorded at their original purchase price. For example, if a company buys Bitcoin for $30,000, that amount remains on the balance sheet regardless of how the market price fluctuates.

However, if the asset’s value drops below the purchase price, companies must record an impairment loss. The problem? If the price later rebounds, the gain cannot be recognized until the asset is sold. This creates a distorted picture of a company’s financial health, especially in the volatile crypto accounting environment.

Key characteristics of cost basis accounting:

- Assets recorded at historical purchase price

- Impairment losses recognized when value drops

- No upward revaluation allowed until sale

- Creates conservative but often misleading valuations

What Is Fair Value Accounting?

Fair value is the agreed price for an asset in a market transaction when a buyer and seller freely negotiate. This approach reflects real-time market conditions and provides a more accurate snapshot of a company’s financial position, especially for crypto accounting purposes.

Key characteristics of fair value accounting:

- Assets marked to current market value

- Gains and losses recognized immediately in earnings

- Reflects both upward and downward price movements

- Provides transparency and timeliness

The Core Difference

| Aspect | Cost Basis | Fair Value |

| Measurement | Historical purchase price | Current market price |

| Impairment | Recognized when value drops | Not applicable; value updated regularly |

| Revaluation | Not allowed until sale | Allowed continuously |

| Earnings Impact | Losses only | Both gains and losses |

| Transparency | Limited | High |

The shift from cost basis to fair value fundamentally changes how crypto assets appear on financial statements. It aligns digital asset reporting with the economic reality of market fluctuations and modern crypto accounting practices.

The FASB Rule Change: A New Era for Crypto Accounting

Background of the Rule

For years, companies and auditors struggled with how to account for cryptocurrencies under U.S. Generally Accepted Accounting Principles (GAAP). Digital assets were classified as indefinite-lived intangible assets, similar to trademarks or goodwill. This classification forced companies to use the cost basis model, leading to impairment losses during market downturns and no recognition of gains during recoveries.

In December 2023, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2023-08, titled “Intangibles—Goodwill and Other—Crypto Assets (Subtopic 350-60)”. This update requires companies to measure certain crypto assets at fair value with changes recognized in net income — a major milestone in crypto accounting evolution.

Effective Date

The rule becomes effective for fiscal years beginning after December 15, 2024, including interim periods within those fiscal years. Early adoption is permitted, allowing forward-thinking companies to implement the change sooner and modernize their crypto accounting systems.

Scope of the Rule

The new standard applies to crypto assets that meet all of the following criteria:

- Are created or reside on a blockchain or distributed ledger.

- Are secured through cryptography.

- Are fungible (interchangeable units).

- Are not issued by the reporting entity or its affiliates.

- Are not securities or financial assets under other GAAP guidance.

This includes major cryptocurrencies like Bitcoin, Ethereum, and stablecoins, but excludes NFTs, tokenized securities, and central bank digital currencies (CBDCs). These distinctions are critical for accurate crypto accounting classification.

Why the Change Was Needed

The Problem with Cost Basis

Under the old rules, companies like Tesla, MicroStrategy, and Coinbase faced significant accounting challenges. When Bitcoin prices dropped, they had to record impairment losses, even if the decline was temporary. When prices rebounded, they couldn’t reverse those losses unless they sold the assets.

This led to:

- Earnings volatility disconnected from actual performance

- Investor confusion due to understated asset values

- Reduced willingness to hold crypto on balance sheets

Broader volatility in corporate crypto holdings is often shaped by capital rotation cycles and liquidity shifts, market dynamics explored in Bitcoin Dominance Chart Explained: How Smart Money Tracks Altcoin Rotation.

The Push for Transparency

Investors and regulators demanded a more transparent and economically accurate method. Fair value accounting provides real-time insight into the value of crypto holdings, aligning financial reporting with market reality.

The FASB’s decision reflects a broader recognition that digital assets are no longer fringe investments but integral components of modern crypto accounting frameworks.

How Fair Value Accounting Works for Crypto

Step 1: Determine Market Price

Companies must use observable market data from active exchanges to determine fair value. For example, if Bitcoin trades at $60,000 on major exchanges, that becomes the fair value for reporting purposes.

Step 2: Record Gains and Losses

Changes in market value are recognized directly in the income statement. If Bitcoin rises from $30,000 to $60,000, the company records a $30,000 unrealized gain. If it falls to $25,000, a $5,000 loss is recorded. This real-time recognition is a cornerstone of modern crypto accounting.

Step 3: Update Balance Sheet

The balance sheet reflects the updated fair value of crypto holdings at each reporting date. This ensures that investors see the most current valuation, a key improvement in crypto accounting transparency.

Step 4: Disclose Methodology

Companies must disclose:

- The valuation techniques used

- The sources of market data

- The classification of gains and losses

This transparency enhances investor confidence and comparability across firms, strengthening the credibility of crypto accounting practices.

Implications for CFOs and Finance Teams

1. Earnings Volatility

Fair value accounting introduces earnings volatility because crypto prices fluctuate daily. CFOs must prepare for swings in reported income, even if the company’s underlying operations remain stable.

However, this volatility reflects real market conditions and provides a more accurate picture of financial performance.

2. Enhanced Transparency

Investors gain clearer insight into a company’s crypto exposure. This transparency can improve investor trust and attract capital from stakeholders who value openness.

3. Strategic Treasury Management

CFOs can now hold crypto assets without fear of permanent impairment losses. This may encourage more companies to diversify their treasuries with digital assets, using them as hedges or liquidity tools.

4. Tax and Compliance Considerations

While the FASB rule affects financial reporting, it does not change tax treatment. Companies must still follow IRS guidelines for crypto taxation, which may differ from crypto accounting recognition.

5. System and Process Upgrades

Finance teams must update accounting systems to handle real-time valuation data, integrate exchange feeds, and automate fair value calculations. Internal controls and audit procedures will also need revision.

Case Studies: How the Rule Impacts Real Companies

Tesla

Tesla famously purchased $1.5 billion in Bitcoin in 2021. Under cost basis accounting, it recorded impairment losses when Bitcoin prices fell, even though the company hadn’t sold any holdings. Under the new rule, Tesla would report both gains and losses as they occur, providing a more accurate reflection of its crypto position.

MicroStrategy

MicroStrategy holds over 200,000 Bitcoin as part of its corporate strategy. The company’s financial statements have been heavily influenced by impairment charges. Under fair value accounting, its balance sheet would show the true market value of its holdings, potentially boosting investor confidence and improving crypto accounting accuracy.

Coinbase

As a crypto-native company, Coinbase’s financials are directly tied to digital asset valuations. The fair value rule aligns its reporting with the nature of its business, reducing discrepancies between operational performance and crypto accounting results.

Benefits of the Fair Value Rule

1. Real-Time Valuation

Fair value accounting ensures that financial statements reflect the current market value of crypto assets, improving accuracy and relevance.

2. Improved Investor Confidence

Transparent reporting builds trust among investors, analysts, and regulators. Stakeholders can make better-informed decisions based on up-to-date information.

3. Reduced Accounting Complexity

The elimination of impairment testing simplifies accounting processes. Companies no longer need to perform periodic impairment analyses or track historical cost layers, streamlining crypto accounting workflows.

4. Encouragement for Corporate Adoption

By removing punitive accounting treatment, the new rule may encourage more companies to hold crypto assets as part of their treasury strategy.

As fair value reporting improves balance-sheet visibility, institutional liquidity channels continue evolving, especially through specialized OTC desks that handle large-scale whale transactions and enhance market efficiency, reinforcing the role of institutional trading infrastructure in crypto markets — Crypto OTC Desks: Cumberland’s Whale Trading Secrets.

Challenges and Risks

1. Market Volatility

Crypto markets are notoriously volatile. Daily price swings can lead to significant fluctuations in reported earnings, requiring CFOs to manage investor expectations carefully.

2. Data Reliability

Determining fair value requires reliable market data. Companies must ensure that their data sources are accurate, consistent, and verifiable.

3. Audit Complexity

Auditors will need to verify fair value measurements, which may involve complex valuation models and third-party data verification.

4. Internal Controls

Organizations must strengthen internal controls around digital asset custody, valuation, and reporting to prevent errors or fraud.

Preparing for Implementation

Step 1: Assess Current Holdings

Identify all crypto assets held by the company and determine whether they fall within the scope of the new rule.

Step 2: Update Accounting Policies

Revise accounting policies to reflect fair value measurement and disclosure requirements.

Step 3: Upgrade Systems

Implement or enhance systems capable of tracking real-time market data and automating fair value calculations.

Step 4: Train Finance Teams

Provide training for accounting staff, auditors, and executives to ensure understanding of the new requirements.

Step 5: Communicate with Stakeholders

Inform investors, analysts, and regulators about the expected impact of the rule change on financial statements.

The Broader Impact on Corporate Finance

A Shift Toward Digital Asset Integration

The fair value rule signals a broader acceptance of digital assets in corporate finance. As accounting barriers fall, more companies may integrate crypto into their operations, from payments to investments.

Enhanced Comparability Across Firms

Standardized fair value reporting allows investors to compare companies’ crypto exposures more easily, improving market efficiency.

Potential Influence on Global Standards

The FASB’s move may influence international accounting bodies like the IASB to adopt similar standards, promoting global consistency in crypto reporting.

The Future of Crypto Accounting

The adoption of fair value accounting is just the beginning. As blockchain technology evolves, new asset classes such as tokenized securities, NFTs, and decentralized finance (DeFi) instruments will challenge existing frameworks.

Future developments may include:

- Expanded guidance for non-fungible and hybrid tokens

- Integration of blockchain-based audit trails

- Real-time financial reporting using distributed ledgers

CFOs who embrace these changes early will position their organizations at the forefront of financial innovation, especially as institutional capital continues flowing into digital assets through venture funding and strategic investments — Crypto Venture Capital Trends: Where Smart Money Is Investing Now.

Additional Considerations for CFOs

Managing Investor Communication

CFOs must proactively communicate how fair value accounting affects reported earnings. Clear explanations in earnings calls, investor presentations, and annual reports can prevent misinterpretation of volatility as operational weakness.

Investors should understand that fluctuations in crypto valuations do not necessarily reflect changes in core business performance. Transparent communication strategies will be essential to maintain confidence.

Integrating Crypto into Risk Management Frameworks

With fair value accounting, crypto assets become more visible on balance sheets, requiring integration into enterprise risk management (ERM) frameworks. CFOs should assess:

- Market risk from price volatility

- Liquidity risk from exchange reliability

- Custodial risk from third-party wallet providers

- Regulatory risk from evolving compliance requirements

Developing a comprehensive risk management policy ensures that crypto exposure aligns with the company’s overall financial strategy.

The Role of Technology and Automation

Automation will play a critical role in implementing fair value accounting efficiently. Advanced accounting software can:

- Pull real-time price feeds from multiple exchanges

- Automate journal entries for unrealized gains and losses

- Generate audit-ready reports

- Integrate with blockchain explorers for transaction verification

Adopting these tools reduces manual errors and enhances audit readiness.

The Importance of Custody Solutions

Secure custody of digital assets remains a top priority. CFOs must evaluate custodial partners based on:

- Security protocols and insurance coverage

- Regulatory compliance

- Transparency in reporting and reconciliation

- Integration with accounting systems

Institutional-grade custody solutions can mitigate operational and security risks while supporting accurate fair value reporting.

Global Perspective: How Other Jurisdictions Handle Crypto Accounting

While the FASB’s rule applies to U.S. GAAP, other jurisdictions are also evolving their standards.

IFRS (International Financial Reporting Standards)

Currently treats crypto as intangible assets, similar to the old U.S. model. However, discussions are underway to consider fair value treatment.

European Union

The European Financial Reporting Advisory Group (EFRAG) is exploring frameworks for digital asset reporting aligned with fair value principles.

Asia-Pacific

Countries like Singapore and Japan are developing hybrid models that combine fair value and cost basis depending on asset type and use case.

The FASB’s decision may accelerate global harmonization, leading to more consistent reporting across borders.

Strategic Opportunities for Businesses

Treasury Diversification

With fair value accounting, companies can hold crypto assets without fear of impairment distortions. This opens opportunities for treasury diversification, allowing firms to allocate a portion of reserves to digital assets as a hedge against inflation or currency risk.

Enhanced Liquidity Management

Crypto assets can serve as liquid instruments for cross-border payments, supplier settlements, or decentralized finance (DeFi) yield strategies. Fair value reporting ensures these assets are accurately reflected in liquidity ratios and financial metrics.

Competitive Advantage

Early adopters of fair value accounting can position themselves as forward-thinking innovators. Transparent crypto reporting can attract tech-savvy investors, partners, and customers who value digital transformation.

Common Misconceptions About the Rule

“Fair Value Means More Risk”

While fair value introduces visible volatility, it doesn’t increase actual risk. It simply reflects market reality more accurately. Companies already exposed to crypto volatility will now show it transparently rather than hiding it under impairment rules.

“It Only Affects Tech Companies”

The rule applies to any company holding crypto assets, regardless of industry. Retailers, manufacturers, and service providers accepting crypto payments or holding digital assets for investment are all impacted.

“It Changes Tax Obligations”

The FASB rule affects financial reporting, not taxation. Companies must still follow IRS rules for recognizing taxable gains or losses upon sale or exchange.

Preparing for the Future: Action Plan for CFOs

Conduct a Crypto Exposure Audit

Identify all digital assets, wallets, and custodians.

Evaluate Accounting Systems

Ensure compatibility with fair value measurement and real-time data integration.

Develop a Disclosure Strategy

Prepare detailed notes for financial statements explaining valuation methods and risk management.

Engage with Auditors Early

Collaborate with auditors to align on valuation methodologies and documentation standards.

Educate the Board and Investors

Provide training sessions to explain the implications of fair value accounting.

Monitor Regulatory Developments

Stay informed about evolving SEC, IRS, and international guidance on digital assets.

Key Takeaways

- Fair value accounting replaces cost basis for eligible crypto assets starting in 2025.

- Earnings will reflect real-time market movements, increasing transparency but also volatility.

- Companies must update systems, policies, and controls to comply with the new rule.

- Investors benefit from clearer, more accurate financial reporting of digital asset holdings.

- The rule marks a major step toward mainstream adoption of crypto in corporate finance.

- CFOs must lead the transition by integrating technology, risk management, and communication strategies.

Frequently Asked Questions (FAQ)

1. What is the difference between fair value and cost basis in crypto accounting?

Cost basis records crypto at its original purchase price, adjusted for impairment. Fair value measures crypto at its current market price at each reporting date. The new rule shifts reporting from historical cost to market-based valuation.

2. Why did crypto accounting rules change?

The previous cost-basis model created an imbalance where companies had to record losses when crypto prices fell but could not recognize gains until selling. The fair value model provides a more accurate picture of real-time asset value.

3. Which accounting standard introduced fair value crypto reporting?

The Financial Accounting Standards Board introduced ASU 2023-08, requiring certain crypto assets to be measured at fair value instead of cost less impairment.

4. When does the new crypto fair value rule take effect?

The rule became effective for fiscal years beginning after December 15, 2024, although early adoption was permitted.

5. How does fair value accounting affect CFOs?

CFOs must now manage greater earnings volatility because unrealized gains and losses from crypto holdings flow directly into net income. This impacts financial planning, investor communication, and risk management.

6. Does fair value accounting apply to all digital assets?

No. It mainly applies to fungible crypto assets that meet FASB’s scope criteria. NFTs and certain tokenized assets may not qualify under the new standard.

7. How will this change impact corporate Bitcoin holdings?

Companies holding Bitcoin can now reflect both price increases and decreases in earnings, giving investors a clearer view of treasury asset performance.

8. Does fair value accounting change crypto taxes?

No. Fair value accounting affects financial reporting, not tax treatment. Tax authorities still rely on cost basis to calculate gains and losses for taxable events.

Conclusion

The shift from cost basis to fair value accounting represents one of the most significant changes in corporate crypto reporting to date. For CFOs, this is not just an accounting update — it’s a strategic transformation.

By aligning financial reporting with market reality, the new FASB rule enhances transparency, improves investor confidence, and paves the way for broader adoption of digital assets in corporate treasuries.

As the financial world continues to evolve, those who adapt early will gain a competitive edge in navigating the intersection of technology, finance, and innovation.

The era of fair value crypto accounting has arrived — and every CFO must be ready to lead through it.